乌兹别克斯坦外商税收政策

1.1

概述

乌兹别克斯坦现行有效的税法典为2020年1月1日开始施行的《乌兹别克斯坦共和国税法典》(简称《税法典》),较以往税法典的主要变化是提高了一般企业所得税和消费税的税率,降低了增值税税率,取消了小型工业区的免税政策和关税减免优惠,调整了税收管理制度。

经济和财政部下属税务委员会是税收系统管理及税款征收的主管部门,各地区也有当地的主管税务机关,直属于税务委员会。负有纳税义务的单位和个人均应按照《税法典》规定的程序向税务机关提交税务登记所需信息。税务机关有权要求纳税人和第三方提交计算和支付税费的文件和信息,并按照《税法典》规定进行税务审计等其他税收控制措施。

图片来源于豆包AI

1.2

主要税赋和税率

1、企业所得税

外资企业主要分为两类情况:

(1)构成常设机构 (PE) 的非居民企业

• 征税范围: 就其在乌境内通过常设机构获得的收入,以及来自境外但与该常设机构有关的收入纳税。

• 税率: 通常适用与居民企业相同的15% 的一般税率(特殊类别为20%),按常设机构的净利润计算。

• 额外税负: 自2022年起,常设机构还需就其净利润缴纳10% 的所得税(类比股息税)。

(2)不构成常设机构的非居民企业

• 征税方式: 采用源泉扣缴(预提税) 方式,由乌方支付款项时扣缴。

• 税率(默认):

▷股息、利息: 10%

▷特许权使用费、租金: 20%

▷国际运输、通信服务: 6%

▷保险保费: 10%

• 重要提示: 如果中国与乌兹别克斯坦的税收协定规定了更低的税率,则优先适用协定税率。

图片来源于豆包AI

2、个人所得税

(1)居民纳税人: 在乌任何12个月内居住满183天的个人被视为税收居民,就其全球所得按12% 的税率纳税。

(2)非居民纳税人: 仅就来源于乌境内的所得纳税,税率也为12%(股息、利息和运费等另有规定)。税款通常由支付方代扣代缴。

3、其他关键税种

• 增值税 (VAT): 自2023年1月1日起,标准税率由15%降至12%。

• 营业税: 这是为小规模纳税人设计的税种,适用于年收入在1亿至10亿苏姆之间的企业。一旦年收入超过10亿苏姆,则必须转为缴纳增值税和所得税。新注册企业可以在两者间选择。

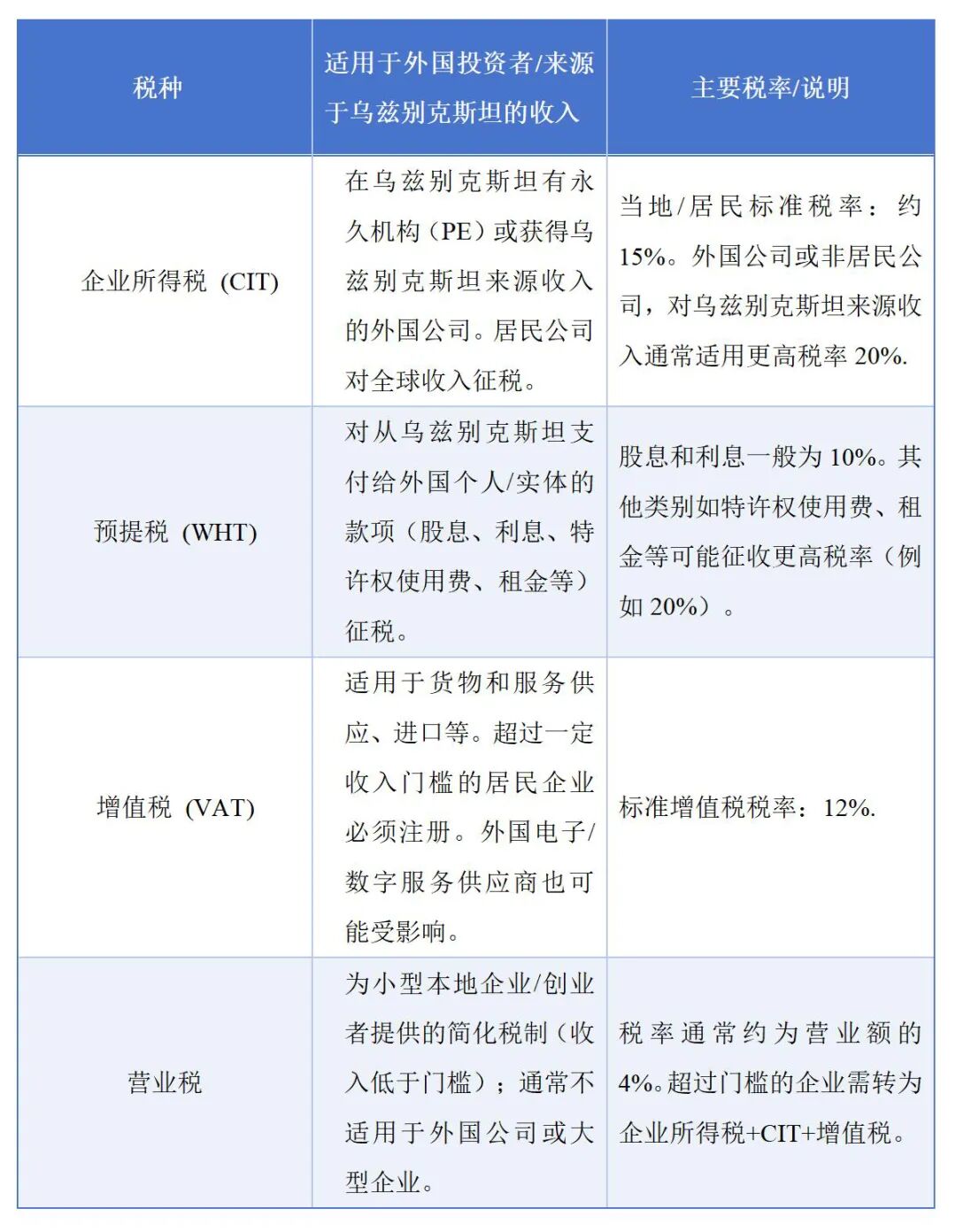

以上信息总结为如下表格:

4、对中资企业的建议

(1)首先判断自身在乌的经营模式是否构成常设机构(如固定场所、项目超过183天等)。

(2)充分利用中乌税收协定,以争取更优惠的预提税税率。

(3)关注营业额规模,以确定是缴纳营业税还是增值税。

(4)在进行商业谈判和定价时,务必考虑税后净收入,因为大部分税款由支付方源头扣缴。

5、合法的减免税措施

(1)乌兹别克斯坦为吸引外国直接投资(FDI)出台了一系列优惠政策,如在财产税、土地税、水资源利用税可能给予豁免,时间3年至7年不等,视具体投资规模与投资地域而定。但可能需满足以下基本条件:外国资本占比不少于33%、硬通货或新生产设备投资、所减免税款需再投入本外资企业等。

(2)在特殊经济区的投资也可享受优惠政策:

①区内注册的实体在乌兹别克斯坦直接投资30万-300万美元,3年免缴土地税、所得税、法人财产税、社会基础设施改造和发展税、统一税(针对小企业)、乌兹别克斯坦财政部预算外学校、职业学院、科学院和医疗机构维修基金扣款等;投资300万-500万美元,优惠期5年;投资500万-1000万美元,优惠期7年;投资1000万美元以上,优惠期10年,10年期满后仍享受所得税和统一税征收减半的优惠。

②为在当地生产商品而从国外进口原料、物资和零部件免征关税(海关手续费除外)。

③区内可流通外汇,即允许以外汇结算和支付。

(3)IT Park综合体园区内的企业和个人享有以下优惠:

• 企业所得税豁免至2040年1月1日

• 个人所得税从12%减至7.5%

• 普通纳税人社会税完全豁免

• 从国外进口的实体服务与数字服务免征增值税

• 进口设备、零组件、技术文件、必要软件免征关税至2028年1月1日

• 园区内企业若出口收入占总营收超过50%,则免征除增值税以外的一切税赋,直至2040年1月1日

• 外资IT服务供应商出口收入超过1000万美元,则免征企业所得税

图片来源于豆包AI

The Foreign Investment Taxation Chapter of Uzbekistan

Taxation Policy for Foreign Investors in Uzbekistan

1.1

Overview

The current effective tax legislation in Uzbekistan is the Tax Code of the Republic of Uzbekistan, which came into force on 1 January 2020. Compared with the previous version, the major changes introduced under the new Tax Code include: an increase in the general corporate income tax and excise tax rates; a reduction in the value-added tax (VAT) rate; the abolition of tax exemptions and customs duty reliefs previously granted to small industrial zones; adjustments to the tax administration system.

The Tax Committee under the Ministry of Economy and Finance is the principal authority responsible for tax administration and collection, with regional tax offices operating under its direct supervision. All entities and individuals subject to taxation are required to provide the necessary registration information to the tax authorities in accordance with the procedures established by the Tax Code. The tax authorities are vested with the power to request documentation and information from taxpayers and third parties concerning the calculation and payment of taxes and fees, and to conduct tax audits as well as other forms of fiscal oversight in line with the provisions of the Tax Code.

1.2

Major Taxes and Applicable Rates

1. Corporate Income Tax (CIT)

For foreign-invested enterprises, the tax treatment depends on whether the non-resident enterprise constitutes a Permanent Establishment (PE) in Uzbekistan:

(1) Non-Resident Enterprises with a Permanent Establishment (PE)

• Tax Scope: Subject to tax on income derived through the PE within Uzbekistan, as well as income from abroad that is connected with the PE.

• Tax Rate: Generally 15%, the same as resident enterprises (20% for certain special categories), calculated on the PE’s net profit.

• Additional Burden: Since 2022, PEs are also required to pay an additional 10% tax on their net profit, similar in effect to a dividend withholding tax.

(2) Non-Resident Enterprises without a Permanent Establishment (PE)

• Method of Taxation: Income is taxed via withholding at source, with the Uzbek payer responsible for deducting the tax upon payment.

• Default Withholding Tax Rates:

▷Dividends and interest: 10%

▷Royalties and rental income: 20%

▷International transportation and communication services: 6%

▷Insurance premiums: 10%

• Important Note: Where a double taxation treaty (DTT) applies (e.g., the China–Uzbekistan DTT), the treaty rates—often lower—take precedence.

2. Personal Income Tax (PIT)

• Resident Individuals: Persons physically present in Uzbekistan for at least 183 days within any 12-month period are deemed tax residents and are taxed on their worldwide income at a flat rate of 12%.

• Non-Resident Individuals: Taxed only on Uzbekistan-source income, also at 12%, though dividends, interest, freight, and other categories may be subject to specific rules. Taxes are typically withheld at source by the payer.

3. Other Key Taxes

• Value-Added Tax (VAT): Effective 1 January 2023, the standard VAT rate was reduced from 15% to 12%.

• Turnover Tax: Designed for small businesses with annual revenue between UZS 100 million and UZS 1 billion. Once revenue exceeds UZS 1 billion, the enterprise must switch to paying VAT and corporate income tax. Newly registered companies may choose between VAT and turnover tax at the outset.

Summary Table: Major Taxes Applicable to Foreign Investors in Uzbekistan

4. Recommendations for Chinese Enterprises

(1) Assess Permanent Establishment (PE) Status – Carefully determine whether the business model in Uzbekistan constitutes a PE (e.g., maintaining a fixed place of business or carrying out projects exceeding 183 days).

(2) Leverage the China–Uzbekistan Double Taxation Agreement (DTA) – Make full use of treaty provisions to secure preferential withholding tax rates.

(3) Monitor Turnover Scale – Closely track annual revenue to determine whether the enterprise should pay turnover tax or VAT.

(4) Incorporate After-Tax Income into Negotiations – During business negotiations and pricing, always factor in net income after taxes, since most taxes are withheld at source by the payer.

5. Lawful Tax Exemptions and Incentives

(1) General FDI Incentives – To attract foreign direct investment (FDI), Uzbekistan offers a range of tax reliefs, including exemptions from property tax, land tax, and water use tax, generally for a period of 3 to 7 years, depending on the scale and geographic location of the investment. Common eligibility requirements may include:

• Foreign capital contribution of at least 33%;

• Investment made in hard currency or through new production equipment;

• Tax savings reinvested into the foreign-invested enterprise itself.

• Special Economic Zones (SEZs) – Investments in SEZs are eligible for substantial tax incentives:

(2) Investments in Special Economic Zones may also enjoy preferential policies:

① Entities registered within the zone that make direct investments in Uzbekistan ranging from USD 300,000 to 3 million are granted a three-year exemption from land tax, corporate income tax, property tax, the social infrastructure development tax, unified tax (for small enterprises), and mandatory contributions to off-budget funds of the Ministry of Finance for schools, vocational colleges, academies, and healthcare institutions. For investments of USD 3–5 million, the exemption period is five years; for USD 5–10 million, the exemption period is seven years; and for investments exceeding USD 10 million, the exemption period is ten years, after which a 50% reduction in corporate income tax and unified tax remains in effect.

② Raw materials, supplies, and components imported from abroad for the purpose of local production are exempt from customs duties, with the exception of customs processing fees.

③ Foreign currency circulation is permitted within the zone, allowing settlements and payments to be made in foreign currency.

(3) Incentives within IT Park Complexes

Enterprises and individuals operating within IT Parks in Uzbekistan are entitled to a broad package of tax incentives, including:

• Corporate Income Tax Exemption until 1 January 2040.

• Reduced Personal Income Tax Rate from 12% to 7.5%.

• Full Exemption from Social Tax for ordinary taxpayers.

• VAT Exemption on imported physical services and digital services from abroad.

• Customs Duty Exemption (until 1 January 2028) on imported equipment, components, technical documentation, and necessary software.

• Full Exemption from All Taxes (except VAT) until 1 January 2040, if more than 50% of a company’s revenue is generated from exports.

• Foreign IT Service Providers generating export revenues exceeding USD 10 million are exempt from corporate income tax.

律师简介

喻冰清律师

简介

• 维思德律师事务所涉外法律事务部部长

• 湖北省律协涉外领军人才律师

• 中国及美国纽约州执业律师

• 工业和信息化部认证数据安全师

经验

• 喻冰清专注于为企业出海提供一站式的法律服务。其对于企业出海北美、欧洲、东南亚、中东、日本等地具有丰富的法律实操经验,擅长互联网泛娱乐业、跨境电商、供应链仓储物流、医疗器械、建材、零部件、化妆品、服装、餐饮等多个行业的出海合规法律服务,为客户境内外战略发展、合规、争议纠纷等复杂法律问题提供切实可行的解决方案。

毛迈律师

简介

• 维思德(深圳)律师事务所律师

• 北京大学 文学学士学位

经验

• 后赴美国纽约深造,经三年学习,获法律博士学位(J.D.),通过美国纽约州法律职业资格考试。在美期间专修公司法、商法、证券法、破产法、信托法,并能熟练运用美国法律数据库进行法律研究。学习期间在北京某顶级律师事务所实习。回国后顺利通过国家法律职业资格考试。

梁思瑾律师

简介

• 维思德(深圳)律师事务所律师

• 伦敦国王学院,获国际商法法学硕士学位

经验

• 在伦敦求学期间,主要研习课程包括企业融资的法律问题、企业并购与收购、公司治理等核心领域。具备扎实的法律专业功底与出色的英语应用能力,能够熟练处理公司法领域各类法律事务、提供专业企业法律顾问服务,并可高效应对与公司法、日常经营相关的涉外法律问题。

• 主要业务领域涵盖:民商事争议解决、公司法、涉外法律服务等。

撰稿|毛 迈

梁思瑾

协作|喻冰清

校对|喻冰清

李 丹

排版|刘晨卉

审核|丁 静

冯颖琼

招贤纳士

JOIN US

未来合伙人 /WISDOM

加盟要求

(1)具有3年以上律师独立执业经历;

(2)有稳定的案源,业务领域发展成熟,能够独立组建专业部门或业务团队;

(3)具有高度的职业道德和诚信,遵守律师职业行为准则;

(4)具有开拓精神及创新意识,较强的团队合作意识;

(5)认同律所文化和发展理念,能推动律所发展和品牌建设。

律师助理 /WISDOM

任职要求

(1)法学专业本科及以上学历、国内知名法学院校毕业者优先。

(2)通过国家司法考试,取得法律资格证A证。

(3)具有较强的写作能力、学习能力、表达能力、沟通能力和团队协作能力。

(4)品行端正,责任心强,有志于长期从事律师职业。

岗位职责

(1)参加法院庭审、非诉调查、项目跟进等律师实务工作;

(2)协助律师做好客户接待工作,进行有效沟通;

(3)在律师指导下协助起草文件,进行案卷整理归档工作;

(4)协助律师进行法律条文和案例检索,法律调查和研究。

@

联系我们

简历请投递至人资邮箱:wuhan@wsdlaw.cn

乌兹别克斯坦外商税收政策

1.1

概述

乌兹别克斯坦现行有效的税法典为2020年1月1日开始施行的《乌兹别克斯坦共和国税法典》(简称《税法典》),较以往税法典的主要变化是提高了一般企业所得税和消费税的税率,降低了增值税税率,取消了小型工业区的免税政策和关税减免优惠,调整了税收管理制度。

经济和财政部下属税务委员会是税收系统管理及税款征收的主管部门,各地区也有当地的主管税务机关,直属于税务委员会。负有纳税义务的单位和个人均应按照《税法典》规定的程序向税务机关提交税务登记所需信息。税务机关有权要求纳税人和第三方提交计算和支付税费的文件和信息,并按照《税法典》规定进行税务审计等其他税收控制措施。

图片来源于豆包AI

1.2

主要税赋和税率

1、企业所得税

外资企业主要分为两类情况:

(1)构成常设机构 (PE) 的非居民企业

• 征税范围: 就其在乌境内通过常设机构获得的收入,以及来自境外但与该常设机构有关的收入纳税。

• 税率: 通常适用与居民企业相同的15% 的一般税率(特殊类别为20%),按常设机构的净利润计算。

• 额外税负: 自2022年起,常设机构还需就其净利润缴纳10% 的所得税(类比股息税)。

(2)不构成常设机构的非居民企业

• 征税方式: 采用源泉扣缴(预提税) 方式,由乌方支付款项时扣缴。

• 税率(默认):

▷股息、利息: 10%

▷特许权使用费、租金: 20%

▷国际运输、通信服务: 6%

▷保险保费: 10%

• 重要提示: 如果中国与乌兹别克斯坦的税收协定规定了更低的税率,则优先适用协定税率。

图片来源于豆包AI

2、个人所得税

(1)居民纳税人: 在乌任何12个月内居住满183天的个人被视为税收居民,就其全球所得按12% 的税率纳税。

(2)非居民纳税人: 仅就来源于乌境内的所得纳税,税率也为12%(股息、利息和运费等另有规定)。税款通常由支付方代扣代缴。

3、其他关键税种

• 增值税 (VAT): 自2023年1月1日起,标准税率由15%降至12%。

• 营业税: 这是为小规模纳税人设计的税种,适用于年收入在1亿至10亿苏姆之间的企业。一旦年收入超过10亿苏姆,则必须转为缴纳增值税和所得税。新注册企业可以在两者间选择。

以上信息总结为如下表格:

4、对中资企业的建议

(1)首先判断自身在乌的经营模式是否构成常设机构(如固定场所、项目超过183天等)。

(2)充分利用中乌税收协定,以争取更优惠的预提税税率。

(3)关注营业额规模,以确定是缴纳营业税还是增值税。

(4)在进行商业谈判和定价时,务必考虑税后净收入,因为大部分税款由支付方源头扣缴。

5、合法的减免税措施

(1)乌兹别克斯坦为吸引外国直接投资(FDI)出台了一系列优惠政策,如在财产税、土地税、水资源利用税可能给予豁免,时间3年至7年不等,视具体投资规模与投资地域而定。但可能需满足以下基本条件:外国资本占比不少于33%、硬通货或新生产设备投资、所减免税款需再投入本外资企业等。

(2)在特殊经济区的投资也可享受优惠政策:

①区内注册的实体在乌兹别克斯坦直接投资30万-300万美元,3年免缴土地税、所得税、法人财产税、社会基础设施改造和发展税、统一税(针对小企业)、乌兹别克斯坦财政部预算外学校、职业学院、科学院和医疗机构维修基金扣款等;投资300万-500万美元,优惠期5年;投资500万-1000万美元,优惠期7年;投资1000万美元以上,优惠期10年,10年期满后仍享受所得税和统一税征收减半的优惠。

②为在当地生产商品而从国外进口原料、物资和零部件免征关税(海关手续费除外)。

③区内可流通外汇,即允许以外汇结算和支付。

(3)IT Park综合体园区内的企业和个人享有以下优惠:

• 企业所得税豁免至2040年1月1日

• 个人所得税从12%减至7.5%

• 普通纳税人社会税完全豁免

• 从国外进口的实体服务与数字服务免征增值税

• 进口设备、零组件、技术文件、必要软件免征关税至2028年1月1日

• 园区内企业若出口收入占总营收超过50%,则免征除增值税以外的一切税赋,直至2040年1月1日

• 外资IT服务供应商出口收入超过1000万美元,则免征企业所得税

图片来源于豆包AI

The Foreign Investment Taxation Chapter of Uzbekistan

Taxation Policy for Foreign Investors in Uzbekistan

1.1

Overview

The current effective tax legislation in Uzbekistan is the Tax Code of the Republic of Uzbekistan, which came into force on 1 January 2020. Compared with the previous version, the major changes introduced under the new Tax Code include: an increase in the general corporate income tax and excise tax rates; a reduction in the value-added tax (VAT) rate; the abolition of tax exemptions and customs duty reliefs previously granted to small industrial zones; adjustments to the tax administration system.

The Tax Committee under the Ministry of Economy and Finance is the principal authority responsible for tax administration and collection, with regional tax offices operating under its direct supervision. All entities and individuals subject to taxation are required to provide the necessary registration information to the tax authorities in accordance with the procedures established by the Tax Code. The tax authorities are vested with the power to request documentation and information from taxpayers and third parties concerning the calculation and payment of taxes and fees, and to conduct tax audits as well as other forms of fiscal oversight in line with the provisions of the Tax Code.

1.2

Major Taxes and Applicable Rates

1. Corporate Income Tax (CIT)

For foreign-invested enterprises, the tax treatment depends on whether the non-resident enterprise constitutes a Permanent Establishment (PE) in Uzbekistan:

(1) Non-Resident Enterprises with a Permanent Establishment (PE)

• Tax Scope: Subject to tax on income derived through the PE within Uzbekistan, as well as income from abroad that is connected with the PE.

• Tax Rate: Generally 15%, the same as resident enterprises (20% for certain special categories), calculated on the PE’s net profit.

• Additional Burden: Since 2022, PEs are also required to pay an additional 10% tax on their net profit, similar in effect to a dividend withholding tax.

(2) Non-Resident Enterprises without a Permanent Establishment (PE)

• Method of Taxation: Income is taxed via withholding at source, with the Uzbek payer responsible for deducting the tax upon payment.

• Default Withholding Tax Rates:

▷Dividends and interest: 10%

▷Royalties and rental income: 20%

▷International transportation and communication services: 6%

▷Insurance premiums: 10%

• Important Note: Where a double taxation treaty (DTT) applies (e.g., the China–Uzbekistan DTT), the treaty rates—often lower—take precedence.

2. Personal Income Tax (PIT)

• Resident Individuals: Persons physically present in Uzbekistan for at least 183 days within any 12-month period are deemed tax residents and are taxed on their worldwide income at a flat rate of 12%.

• Non-Resident Individuals: Taxed only on Uzbekistan-source income, also at 12%, though dividends, interest, freight, and other categories may be subject to specific rules. Taxes are typically withheld at source by the payer.

3. Other Key Taxes

• Value-Added Tax (VAT): Effective 1 January 2023, the standard VAT rate was reduced from 15% to 12%.

• Turnover Tax: Designed for small businesses with annual revenue between UZS 100 million and UZS 1 billion. Once revenue exceeds UZS 1 billion, the enterprise must switch to paying VAT and corporate income tax. Newly registered companies may choose between VAT and turnover tax at the outset.

Summary Table: Major Taxes Applicable to Foreign Investors in Uzbekistan

4. Recommendations for Chinese Enterprises

(1) Assess Permanent Establishment (PE) Status – Carefully determine whether the business model in Uzbekistan constitutes a PE (e.g., maintaining a fixed place of business or carrying out projects exceeding 183 days).

(2) Leverage the China–Uzbekistan Double Taxation Agreement (DTA) – Make full use of treaty provisions to secure preferential withholding tax rates.

(3) Monitor Turnover Scale – Closely track annual revenue to determine whether the enterprise should pay turnover tax or VAT.

(4) Incorporate After-Tax Income into Negotiations – During business negotiations and pricing, always factor in net income after taxes, since most taxes are withheld at source by the payer.

5. Lawful Tax Exemptions and Incentives

(1) General FDI Incentives – To attract foreign direct investment (FDI), Uzbekistan offers a range of tax reliefs, including exemptions from property tax, land tax, and water use tax, generally for a period of 3 to 7 years, depending on the scale and geographic location of the investment. Common eligibility requirements may include:

• Foreign capital contribution of at least 33%;

• Investment made in hard currency or through new production equipment;

• Tax savings reinvested into the foreign-invested enterprise itself.

• Special Economic Zones (SEZs) – Investments in SEZs are eligible for substantial tax incentives:

(2) Investments in Special Economic Zones may also enjoy preferential policies:

① Entities registered within the zone that make direct investments in Uzbekistan ranging from USD 300,000 to 3 million are granted a three-year exemption from land tax, corporate income tax, property tax, the social infrastructure development tax, unified tax (for small enterprises), and mandatory contributions to off-budget funds of the Ministry of Finance for schools, vocational colleges, academies, and healthcare institutions. For investments of USD 3–5 million, the exemption period is five years; for USD 5–10 million, the exemption period is seven years; and for investments exceeding USD 10 million, the exemption period is ten years, after which a 50% reduction in corporate income tax and unified tax remains in effect.

② Raw materials, supplies, and components imported from abroad for the purpose of local production are exempt from customs duties, with the exception of customs processing fees.

③ Foreign currency circulation is permitted within the zone, allowing settlements and payments to be made in foreign currency.

(3) Incentives within IT Park Complexes

Enterprises and individuals operating within IT Parks in Uzbekistan are entitled to a broad package of tax incentives, including:

• Corporate Income Tax Exemption until 1 January 2040.

• Reduced Personal Income Tax Rate from 12% to 7.5%.

• Full Exemption from Social Tax for ordinary taxpayers.

• VAT Exemption on imported physical services and digital services from abroad.

• Customs Duty Exemption (until 1 January 2028) on imported equipment, components, technical documentation, and necessary software.

• Full Exemption from All Taxes (except VAT) until 1 January 2040, if more than 50% of a company’s revenue is generated from exports.

• Foreign IT Service Providers generating export revenues exceeding USD 10 million are exempt from corporate income tax.

律师简介

喻冰清律师

简介

• 维思德律师事务所涉外法律事务部部长

• 湖北省律协涉外领军人才律师

• 中国及美国纽约州执业律师

• 工业和信息化部认证数据安全师

经验

• 喻冰清专注于为企业出海提供一站式的法律服务。其对于企业出海北美、欧洲、东南亚、中东、日本等地具有丰富的法律实操经验,擅长互联网泛娱乐业、跨境电商、供应链仓储物流、医疗器械、建材、零部件、化妆品、服装、餐饮等多个行业的出海合规法律服务,为客户境内外战略发展、合规、争议纠纷等复杂法律问题提供切实可行的解决方案。

毛迈律师

简介

• 维思德(深圳)律师事务所律师

• 北京大学 文学学士学位

经验

• 后赴美国纽约深造,经三年学习,获法律博士学位(J.D.),通过美国纽约州法律职业资格考试。在美期间专修公司法、商法、证券法、破产法、信托法,并能熟练运用美国法律数据库进行法律研究。学习期间在北京某顶级律师事务所实习。回国后顺利通过国家法律职业资格考试。

梁思瑾律师

简介

• 维思德(深圳)律师事务所律师

• 伦敦国王学院,获国际商法法学硕士学位

经验

• 在伦敦求学期间,主要研习课程包括企业融资的法律问题、企业并购与收购、公司治理等核心领域。具备扎实的法律专业功底与出色的英语应用能力,能够熟练处理公司法领域各类法律事务、提供专业企业法律顾问服务,并可高效应对与公司法、日常经营相关的涉外法律问题。

• 主要业务领域涵盖:民商事争议解决、公司法、涉外法律服务等。

撰稿|毛 迈

梁思瑾

协作|喻冰清

校对|喻冰清

李 丹

排版|刘晨卉

审核|丁 静

冯颖琼

招贤纳士

JOIN US

未来合伙人 /WISDOM

加盟要求

(1)具有3年以上律师独立执业经历;

(2)有稳定的案源,业务领域发展成熟,能够独立组建专业部门或业务团队;

(3)具有高度的职业道德和诚信,遵守律师职业行为准则;

(4)具有开拓精神及创新意识,较强的团队合作意识;

(5)认同律所文化和发展理念,能推动律所发展和品牌建设。

律师助理 /WISDOM

任职要求

(1)法学专业本科及以上学历、国内知名法学院校毕业者优先。

(2)通过国家司法考试,取得法律资格证A证。

(3)具有较强的写作能力、学习能力、表达能力、沟通能力和团队协作能力。

(4)品行端正,责任心强,有志于长期从事律师职业。

岗位职责

(1)参加法院庭审、非诉调查、项目跟进等律师实务工作;

(2)协助律师做好客户接待工作,进行有效沟通;

(3)在律师指导下协助起草文件,进行案卷整理归档工作;

(4)协助律师进行法律条文和案例检索,法律调查和研究。

@

联系我们

简历请投递至人资邮箱:wuhan@wsdlaw.cn